```{r}

library(tidyverse)

library(lubridate); library(tsibble)

library(readxl)

url <- "https://www.newyorkfed.org/medialibrary/interactives/sce/sce/downloads/data/frbny-sce-data.xls"

destfile <- "frbny_sce_data.xls"

curl::curl_download(url, destfile)

Inflation.Expectations <- read_excel(destfile, sheet=4, skip=3) %>%

rename(date = 1) %>%

mutate(date = yearmonth(parse_date_time(date, orders = "%Y%m")))

```The slides are here..

Our ninth class meeting will focus on Chapter 3 and Chapter 4 of Forecasting: Principles and Practice [3rd edition].

All of the data for today, including computations, can be acquired using

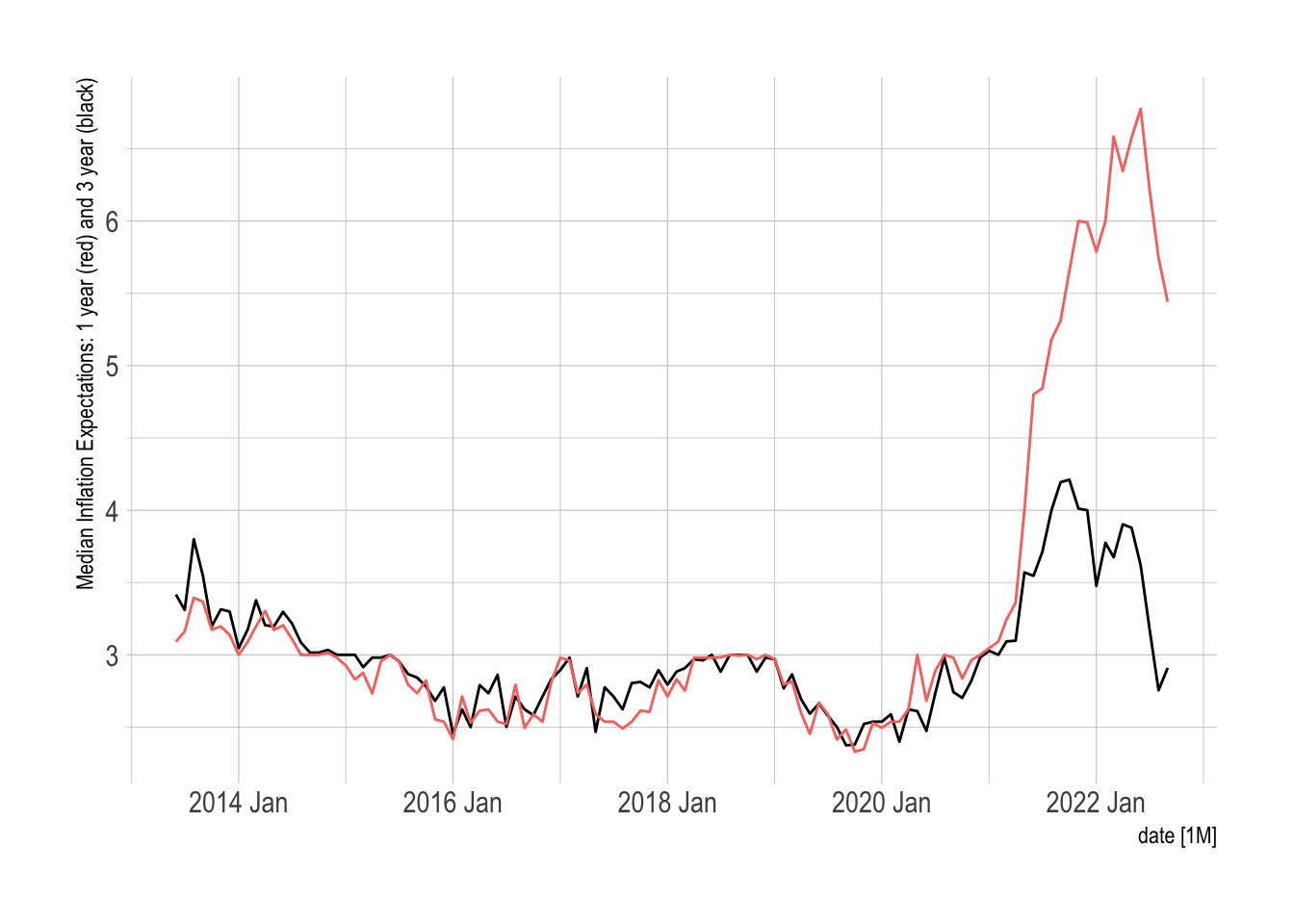

load(url("https://github.com/robertwwalker/xaringan/raw/master/CMF-Week-9/data/FullWorkspace.RData"))Inflation Expectations

```{r}

library(fpp3)

Inflation.Expectations %>%

as_tsibble(index=date) %>%

autoplot(`Median three-year ahead expected inflation rate`) +

geom_line(aes(y=Inflation.Expectations$`Median one-year ahead expected inflation rate`, color="red")) +

hrbrthemes::theme_ipsum() + guides(color = "none") + labs(y="Median Inflation Expectations: 1 year (red) and 3 year (black)")

```

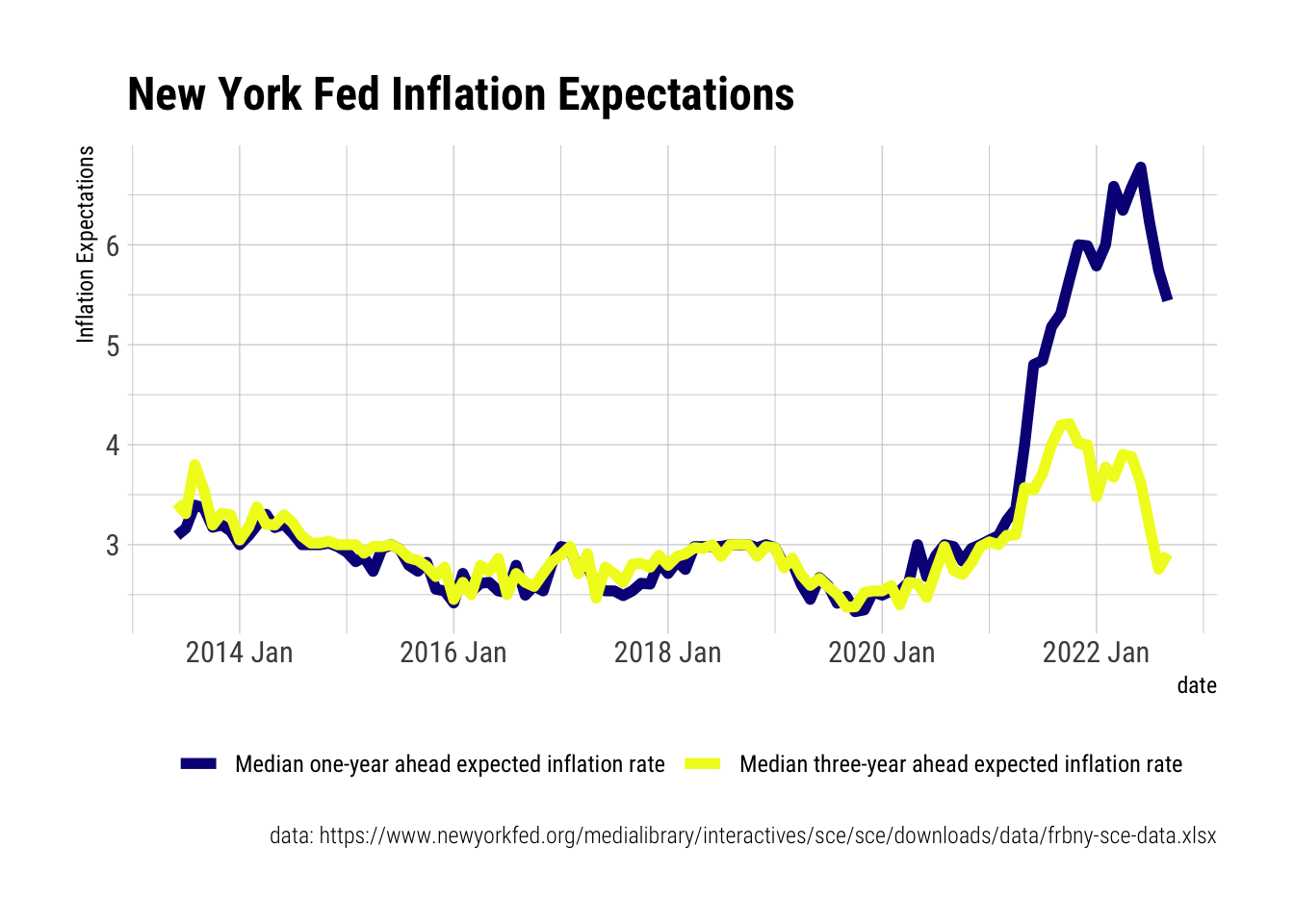

A nicer plot.

```{r}

Inflation.Expectations %>%

select(1:3) %>%

pivot_longer(c(2:3)) %>%

mutate(Variable = name) %>%

ggplot(aes(x=date, y=value, color=Variable)) +

geom_line(size=2) +

scale_color_viridis_d(option="C") +

hrbrthemes::theme_ipsum_rc() +

theme(legend.position = "bottom") +

labs(y="Inflation Expectations",

color="",

title="New York Fed Inflation Expectations",

caption = "data: https://www.newyorkfed.org/medialibrary/interactives/sce/sce/downloads/data/frbny-sce-data.xlsx")

```

Decompositions

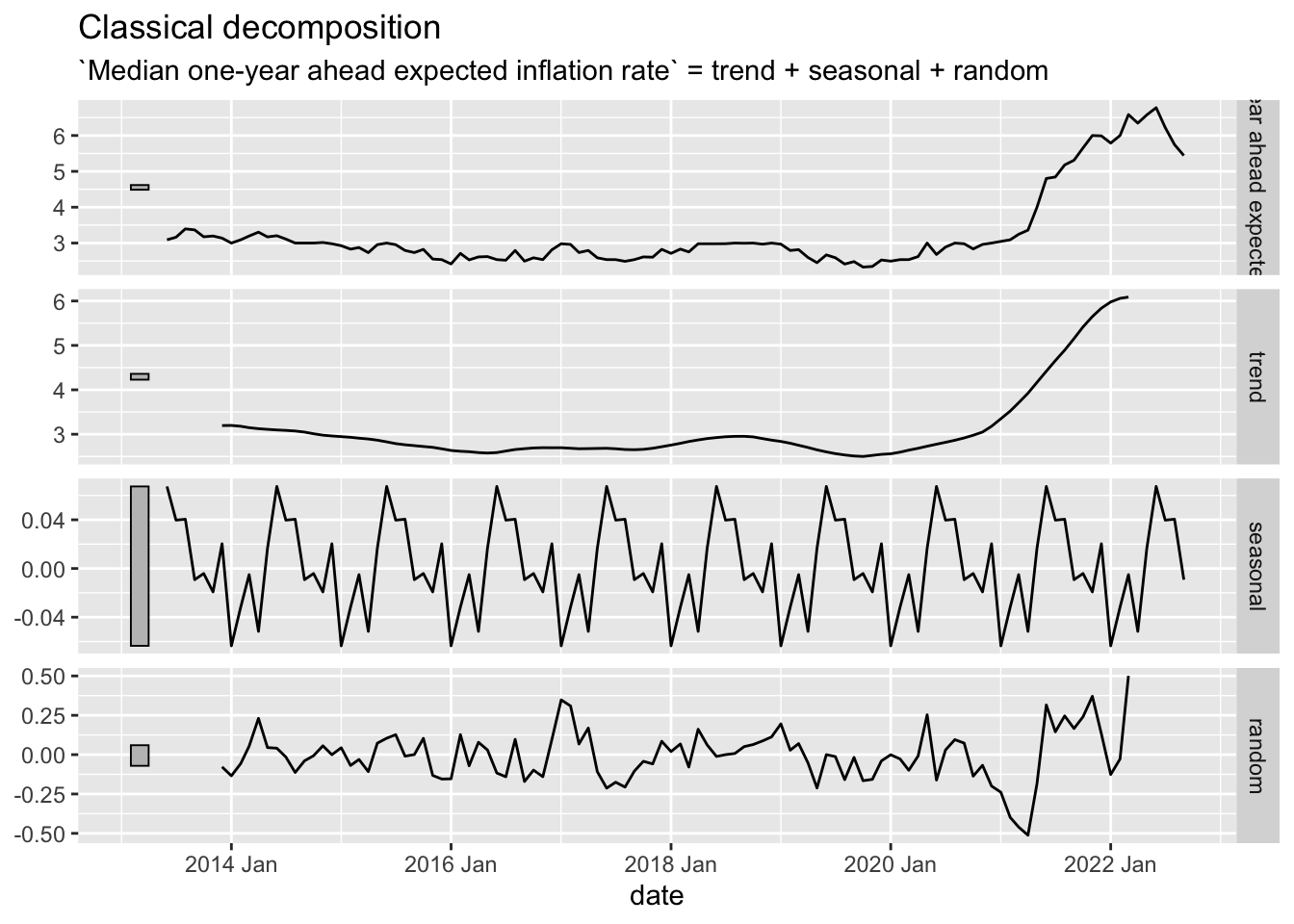

Classical Decomposition

The key difference between the two decompositions, and there are others, is the existence [or lack thereof] of a window. In the classical decomposition, there is almost no flexibility.

```{r}

Inflation.Expectations %>%

as_tsibble(index=date) %>%

model(stl = classical_decomposition(`Median one-year ahead expected inflation rate` ~ season(12))) %>%

components() %>%

autoplot()

```

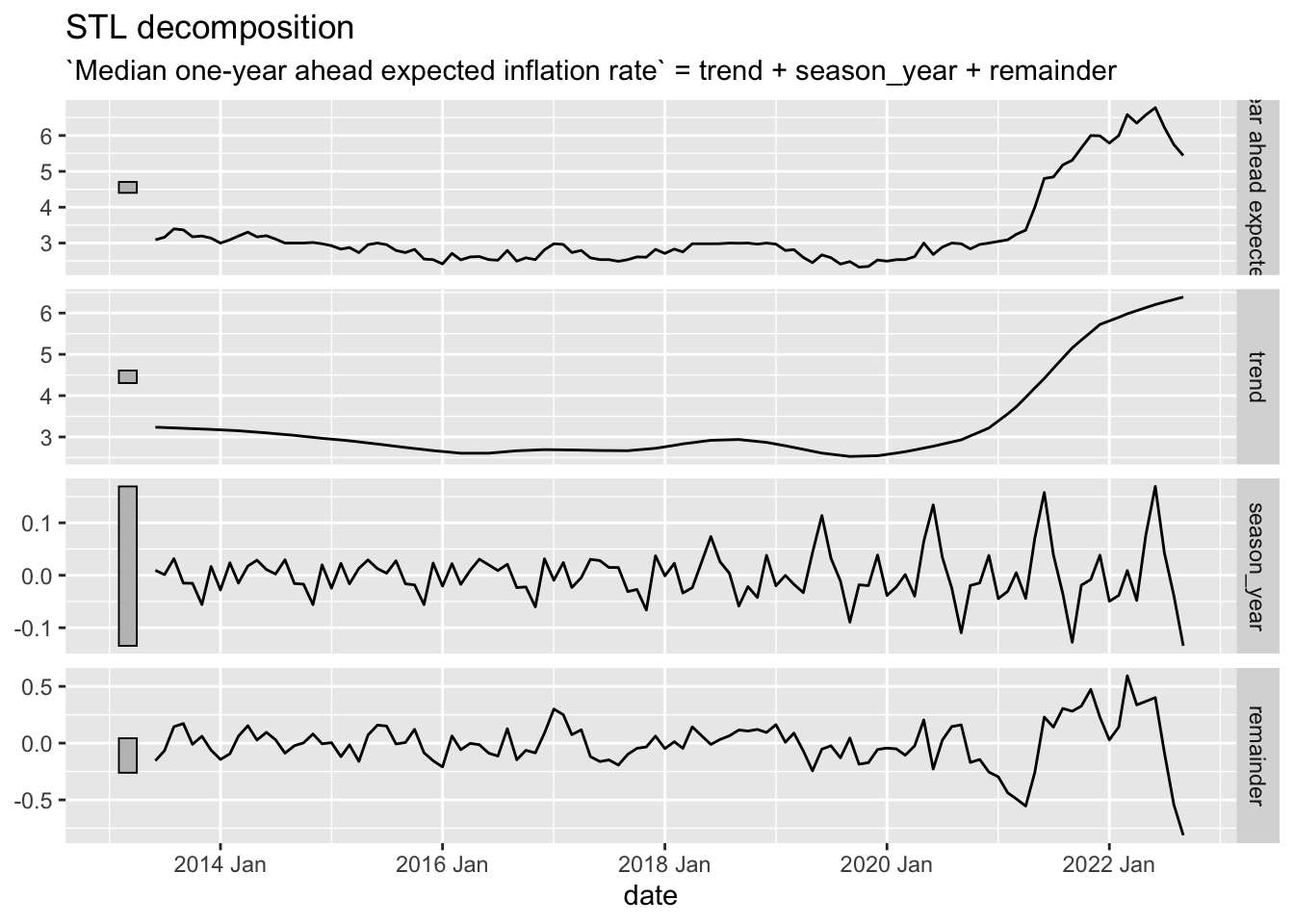

STL Decomposition

The key new element to the STL decomposition is the window argument. Over how many time periods should the trend/season be calculated. If one wishes to average over all periods, window="periodic" is the necessary syntax.

```{r}

Inflation.Expectations %>%

as_tsibble(index=date) %>%

model(STL(`Median one-year ahead expected inflation rate`)) %>%

components() %>%

autoplot()

```